2020/21 Federal Budget

1. Personal income tax changes

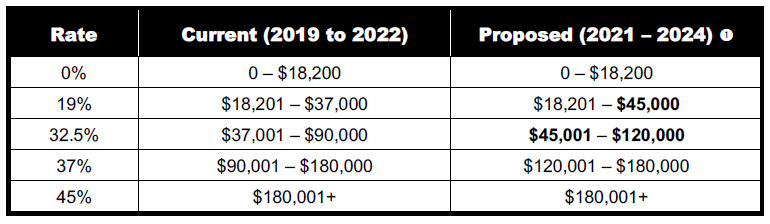

1.1 Changes to personal income tax rates

The Government has announced that it will bring forward changes to the personal income tax rates that were due to apply from 1 July 2022, so that these changes now apply from 1 July 2020 (i.e., from the 2021 income year). These changes involve:

• increasing the upper threshold of the 19% personal income tax bracket from $37,000 to $45,000; and

• increasing the upper threshold of the 32.5% personal income tax bracket from $90,000 to $120,000.

These changes are illustrated in the following table (which excludes the Medicare Levy).

The Government advised that the personal income tax rate changes that have already been legislated, effective from 1 July 2024 (i.e., from the 2025 income year), remain unchanged. These involve abolishing the 37% personal income tax bracket, reducing the 32.5% personal income tax bracket to 30%, and increasing the upper threshold of the reduced 30% tax bracket from $120,000 to $200,000.

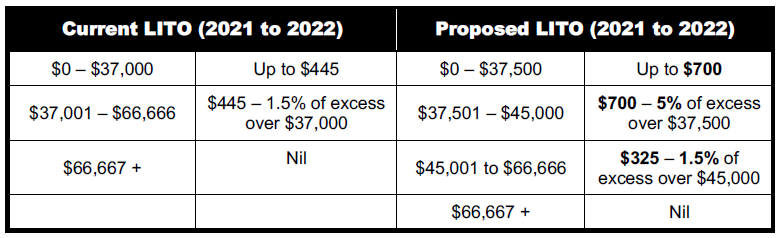

1.2 Changes to the Low Income Tax Offset (‘LITO’)

The Government announced that it will also bring forward the changes that were proposed to the LITO from 1 July 2022, so that they will now apply from 1 July 2020 (i.e., from the 2021 income year), as follows:

• The maximum LITO will be increased from $445 to $700.

• The increased (maximum) LITO will be reduced at a rate of 5 cents per dollar, for taxable incomes between $37,500 and $45,000.

• The LITO will be reduced at a rate of 1.5 cents per dollar, for taxable incomes between

$45,000 and $66,667.

Note that, the Government also announced that the current Low and Middle Income Tax Offset(‘LAMITO’) would continue to apply for the 2021 income year (which is available in addition to the LITO for eligible taxpayers). For example, the maximum LAMITO of $1,080 will be available to taxpayers with taxable incomes of between $48,000 and $90,000 in the 2021 income year.

2. Changes affecting business taxpayers

2.1 Expanding access to Small Business Tax Concessions

The Government has announced that it will expand the concessions available to Medium Sized Entities to provide access to up to ten Small Business Concessions.

For this purpose, a Medium Sized Entity is an entity with an aggregated annual turnover of at least $10 million and (less than) $50 million.

The expanded concessions will apply in three phases, as follows:

1. From 1 July 2020, eligible businesses will be able to immediately deduct certain start-up expenses and certain prepaid expenditure.

2. From 1 April 2021, eligible businesses will be exempt from FBT on car parking and multiple work-related portable electronic devices, such as phones or laptops, provided to employees.

3. From 1 July 2021:

- Eligible businesses will be able to access the simplified trading stock rules, remit pay as you go (PAYG) instalments based on GDP adjusted notional tax and settle excise duty and excise-equivalent customs duty monthly on eligible goods.

- Eligible businesses will generally have a two-year amendment period apply to income tax assessments for income years starting from 1 July 2021.

- The Commissioner of Taxation’s power to create a simplified accounting method

determination for GST purposes will be expanded to apply to businesses below the $50 million aggregated annual turnover threshold.

2.2 JobMaker Hiring Credit

The Government will introduce a JobMaker Hiring Credit to incentivise businesses to take on additional young job seekers.

From 7 October 2020, eligible employers will be able to claim $200 a week for each additional eligible employee they hire aged 16 to 29 years old and $100 a week for each additional eligible employee aged 30 to 35 years old. New jobs created until 6 October 2021 will attract the credit for up to 12 months from the date the new position is created.

The JobMaker Hiring Credit will be claimed quarterly in arrears by the employer from the ATO from 1 February 2021. Employers will need to report quarterly that they meet the eligibility criteria.

The amount of the credit is capped at $10,400 for each additional new position created. Furthermore, the total credit claimed by an employer cannot exceed the amount of the increase in payroll for the reporting period in question (see employer eligibility requirements below).

2.2.1 Who is an eligible employee?

Employees may be employed on a permanent, casual or fixed term basis.

To be an ‘eligible employee’, the employee must:

- Employees may be employed on a permanent, casual or fixed term basis.

To be an ‘eligible employee’, the employee must:- 16 to 29 years old, to attract the payment of $200 per week; or

- 30 to 35 years old to attract the payment of $100 per week;

- have worked at least 20 paid hours per week on average for the full weeks they were employed over the reporting period;

- have commenced their employment during the period from 7 October 2020 to 6 October 2021;

- have received the JobSeeker Payment, Youth Allowance (Other), or Parenting Payment for at least one month within the past three months before they were hired; and

- be in their first year of employment with this employer and must be employed for the period that the employer is claiming for them.

Certain exclusions apply, including employees for whom the employer is also receiving a wage subsidy under another Commonwealth program.

2.2.2 Who is an eligible employer?

An employer is able to access the JobMaker Hiring Credit if the employer:

- has an ABN;

- is up to date with tax lodgement obligations;

- is registered for Pay As You Go withholding;

- is reporting through Single Touch Payroll;

- is claiming in respect of an ‘eligible employee’;

- has kept adequate records of the paid hours worked by the employee they are claiming the hiring credit in respect of; and

- is able to demonstrate that the credit is claimed in respect of an additional job that has been created. Broadly, there must be an increase in the business’ total employee headcount and also in the payroll of the business for the reporting period (based on a comparison over a specified reference period).

Employers do not need to satisfy a fall in turnover test to access the JobMaker Hiring Credit.

Certain employers are excluded, including those who are claiming the JobKeeper payment.

New employers created after 30 September 2020 are not eligible for the first employee hired but are (potentially) eligible for the second and subsequent eligible hires.

2.3 Tax-free business support grants

The Government has announced that the Victorian Government’s Business Support Grants for small and medium businesses, as announced on 13 September 2020, are non-assessable, nonexempt income for tax purposes. The Government may extend this arrangement to similar future grants from all States and Territories on an application basis. Eligibility for this treatment will be limited to grants announced on or after 13 September 2020 and for payments made between 13 September 2020 and 30 June 2021.

2.4 Uncapped immediate write-off for depreciable assets

The Government has announced it will introduce the following changes to the Capital Allowance provisions:

(a) Businesses with an aggregated annual turnover of less than $5 billion will be able to claim an immediate deduction (what the Budget terms as ‘full expensing’) for the full (uncapped) cost of an eligible depreciable asset, in the year the asset is first used or is installed ready for use, where the following requirements are satisfied:

- The asset was acquired from 7:30pm AEDT on 6 October 2020 (i.e., Budget night).

- The asset was first used or installed ready for use by 30 June 2022.

- The asset is a new depreciable asset or is the cost of an improvement to an existing eligible asset, unless the taxpayer qualifies as a small or medium sized business (i.e., for these purposes, a business with an aggregated annual turnover of less than $50 million), in which case the asset can be second-hand.

(b) As is currently legislated, businesses with aggregated annual turnover between $50 million and $500 million can still deduct the cost of eligible second-hand assets costing less than $150,000 that are purchased from 2 April 2019 and first used or installed ready for use between 12 March 2020 and 31 December 2020 under the enhanced instant asset write-off. The Government has announced that it will extend the period in which such assets must first be used or installed ready for use by 6 months, until 30 June 2021.

(c) Small businesses (i.e., with aggregated annual turnover of less than $10 million) can deduct the balance of their simplified depreciation pool at the end of the income year while full expensing applies (i.e., up to 30 June 2022). Furthermore, the provisions which prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended.

3. Changes affecting companies

3.1 Temporary loss carry back for eligible companies

The Government has announced that it will introduce measures to allow companies with a turnover mof less than $5 billion to carry back losses from the 2020, 2021 or 2022 income years to offset previously taxed profits made in or after the 2019 income year.

This will allow such companies to generate a refundable tax offset in the year in which the loss is made. The tax refund is limited by requiring that the amount carried back is not more than the earlier taxed profits and that the carry back does not generate a franking account deficit.

The tax refund will be available on election by eligible companies when they lodge their tax returns for the 2021 and 2022 income years. Note that, companies that do not elect to carry back losses under this measure can still carry losses forward as normal.

3.2 Clarifying the corporate residency test

The corporate residency rules are fundamental to determining a company’s Australian income tax liability. The Government will amend the law to provide that a company that is incorporated offshore will be treated as an Australian tax resident if it has a ‘significant economic connection to Australia’.

This test will be satisfied where both the company’s core commercial activities are undertaken in Australia and its central management and control is in Australia. This change will ensure the principles governing the residency of foreign incorporated companies will reflect the position prior to the 2016 court decision in Bywater Investments Limited & Ors v. FCT; Hua Wang Bank Berhad v FCT [2016] HCA 45 (after this decision the ATO withdrew Taxation Ruling (‘TR’) 2004/15 and later released TR 2018/5, incorporating the High Court’s residency test).

The measure will have effect from the first income year after the date of Royal Assent of the enabling legislation, but taxpayers will have the option of applying the new law from 15 March 2017.

3.3 Meetings conducted via virtual attendance

In order to reduce regulatory barriers, the Government has announced it will undertake public consultation on making permanent changes to the Corporations Act 2001. These changes would allow companies to call and conduct meetings electronically (with a quorum achievable through virtual attendance of shareholders and officers) and also to provide certainty that company officers can electronically execute a document.

4. FBT changes

4.1 FBT exemption for retraining and reskilling employees

From 2 October 2020, the Government will introduce an FBT exemption for retraining and reskilling benefits provided by an employer to redundant, or soon to be redundant, employees, where the benefits may not be related to their current employment (e.g., where an employer retrains a sales assistant in web design in order to redeploy them to an online marketing role in the business).

This measure is designed to encourage employers to assist redundant workers to transition to new employment opportunities within or outside an employer’s business (e.g., to prepare such employees for their next career), without triggering an FBT liability.

Currently, FBT is payable if an employer provides training to redundant, or soon to be redundant, employees and that training does not have a sufficient connection to their current employment.

The FBT exemption will not extend to retraining acquired by way of a salary packaging arrangement. It will also not be available for Commonwealth supported places at universities (which already receive a benefit) or extend to repayments towards Commonwealth student loans.

The Government will also consult on allowing an individual to claim a tax deduction for education and training expenses they incur themselves, where the expense is not related to their current employment (e.g., where the expense relates to future employment).

4.2 Reducing the compliance burden of FBT record keeping

The Government will provide the ATO with the power to allow employers to rely on existing corporate records, rather than employee declarations and other prescribed records, to finalise their FBT returns. The measure will have effect from the start of the first FBT year (i.e., on 1 April) after the date of Royal Assent of the relevant legislation.

Currently, the FBT legislation prescribes the form that certain records must take, and forces employers (and in some cases employees) to create additional records in order to comply with FBT obligations.

This measure will allow employers (with what the Commissioner determines as adequate alternative records) to rely on existing corporate records, removing the need to complete additional records. This will reduce compliance costs for employers, while maintaining the integrity of the FBT system.

5. Other budget announcements

5.1 Removing CGT for ‘granny flat arrangements’

A targeted CGT exemption will apply from 1 July 2021 (subject to the passing of legislation), for ‘granny flat arrangements’. Broadly, these involve older Australians or people with disabilities transferring their home or the proceeds from the sale of their home (and/or other assets) to their adult children or other trusted persons in return for the promise of ongoing housing and care.

Under this exemption, CGT will not apply to the creation, variation or termination of a formal written granny flat arrangement providing accommodation for older Australians or people with disabilities.

This change will only apply to agreements that are entered into because of family relationships or other personal ties and will not apply to commercial rental arrangements.

This measure is consistent with the recommendations made in the Board of Taxation’s Review of Granny Flat Arrangements, the Government’s National Plan to Respond to the Abuse of Older Australians announced on 19 March 2019, and the 2017 Australian Law Reform Commission’s Report: Elder Abuse — A National Legal Response.

5.2 Superannuation reforms

The Government will provide $159.6 million over four years from 2020/21 to implement reforms to improve outcomes for superannuation fund members.

Currently, structural flaws in the superannuation system mean that unnecessary fees and insurance premiums are paid on multiple accounts, members pay too much in super fees, underperforming products are costing members in lost retirement savings, and there is inadequate transparency on how funds are spending members’ money.

From 1 July 2021, the proposed reforms will make the system better for members in four key ways:

- Your superannuation follows you – An existing superannuation account will be ‘stapled’ to a member to avoid the creation of a new account when that person changes their employment.

- Empowering members – A new, interactive, online YourSuper comparison tool will help members decide which super product best meets their needs.

- Holding funds to account for underperformance – MySuper products will be subject to an annual performance test. Funds that underperform will need to inform their members. Funds that fail two consecutive underperformance tests will not be permitted to receive new members unless their performance improves. By 1 July 2022, annual performance tests will be extended to other superannuation products.

- Increased accountability and transparency – The Government will strengthen obligations on superannuation trustees to ensure their actions are consistent with members’ retirement savings being maximised. For example, trustees will be required to comply with a new duty to act in the best financial interests of members.

5.3 Clarifying income tax exemptions for individuals engaged by the IMF and the World Bank group

The Government will clarify privileges and immunities, including income tax exemptions, available to Australian individuals performing short term missions on behalf of the International Monetary Fund (‘IMF’) and three institutions of the World Bank Group (‘WBG’). The measure will apply retrospectively from 1 July 2017.

This measure will clarify that Australian short-term experts are entitled to an exemption from income tax for their relevant income from the organisations. This aligns Australia’s domestic legislative framework with its international obligations and provides certainty for taxpayers. This outcome is consistent with Australia’s longstanding support for and contributions to the IMF and the WBG.

5.4 Additional funding to address serious and organised crime in the tax and superannuation system

The Government will provide $15.1 million to the ATO to target serious and organised crime in the tax and superannuation systems. This extends the 2017/18 Budget measure Additional funding for addressing serious and organised crime in the tax system by a further two years to 30 June 2023.

5.5 Supporting the mental health of Australians in small business – COVID-19 response package

The Government will provide $7 million in 2020/21 to support the mental health and financial wellbeing of small businesses impacted by COVID-19, including:

- $4.3 million to provide free, accessible and tailored support for small business owners by expanding Beyond Blue’s New Access program in partnership with the Australian Small Business and Family Enterprise Ombudsman; and

- $2.2 million to expand a free accredited professional development program that builds the mental health literacy of trusted business advisers so that they can better support small business owners in times of distress, delivered through Deakin University.

5.6 Insolvency reforms to support small business

The Government will implement certain insolvency reforms, effective from 1 January 2021 (subject to the passing of legislation) to support small business, including the following:

- The introduction of a new streamlined process to enable eligible incorporated small businesses (broadly, those with liabilities of less than $1 million) in financial distress to restructure their debt.

- Simplifying the liquidation process for eligible incorporated small businesses (to allow faster and lower-cost liquidations, increasing returns for creditors and employees).

- Support for the insolvency sector (to ensure it can respond effectively to increased demand and to the needs of small business).

Currently, the insolvency system faces a number of challenges. These include an increase in the number of businesses in financial distress due to COVID-19, a ‘one-size-fits-all’ system, and high costs and lengthy processes that can prevent distressed small businesses from engaging with the insolvency system early thereby reducing their opportunity to restructure and survive.

Temporary insolvency and bankruptcy protections that were introduced in March 2020 to provide relief for businesses impacted by COVID-19 are due to expire on 31 December 2020 (e.g., under these measures, directors are temporarily relieved from personal liability for trading while insolvent). However, the number of companies being put into external administration is expected to increase significantly, putting additional stress on the system. Therefore, the above proposed reforms will help more businesses to successfully get to the other side of the crisis.